Mumbai,August 01, 2024.

Tata Motors Ltd.(TML) announced its results for quarter ending June 30, 2024.

| Q1FY25 | Consolidated (₹ Cr Ind AS) | Jaguar Land Rover (£m, IFRS) | Tata Commercial Vehicles (₹Cr, Ind AS) | Tata Passenger Vehicles (₹Cr, Ind AS) | |||||||

| FY25 | Vs. PY | FY25 | Vs. PY | FY25 | Vs. PY | FY25 | Vs. PY | ||||

| Revenue | 108,048 | 5.7% | 7,273 | 5.4% | 17,849 | 5.1% | 11,847 | (7.7)% | |||

| EBITDA (%) | 14.4 | – | 15.8 | (50) bps | 11.6 | 220 bps | 5.8 | 50 bps | |||

| EBIT (%) | 8.4 | 30 bps | 8.9 | 30 bps | 8.9 | 240 bps | 0.3 | (70) bps | |||

| PBT (bei) | 8,828 | ₹3,287crs | 693 | £258m | 1,535 | ₹598crs | 173 | ₹(13) crs | |||

Tata Motors Consolidated:

TML delivered astrong performance in Q1 FY25 with revenues at ₹108.0K Cr (up 5.7%), EBIT of ₹9.1KCr(+ ₹0.9KCr), EBIT margin of 8.4% (+30bps).JLR revenues grew by 5.4% to £7.3bwithEBIT margins of 8.9% (+30bps) driven by favourable volume, mix and material cost improvements. CV revenues grew by 5.1% to ₹17.8K Crand EBIT margins improved to 8.9% (+240 bps) benefiting from better realizations and material cost savings. PV revenues declined by 7.7%, reflecting the challenging market conditions but EBITDA at 5.8% was up +50bpsdriven by material cost reductions. Overall PBT(bei) improved by ₹3.3KCr to ₹8.8KCron lower interest outflow, favourable currency and commodity movements. Net Profit was ₹5.7KCr (+₹ 2.4K cr yoy).

Corporate actions:

The Board has approved the Scheme of Demerger of Tata Motors into two separate listed companies and is expected to conclude in the next 12 to 15 months. The merger of Tata Motors Finance with Tata Capital is also underway and expected to conclude over the course of next 9 to 12 months.We also expect the process of cancellation of DVR and issuance of ORD shares to be completed in about 2 months. These transactions are subject to necessary approvals

Looking Ahead:

Global demand is likely to remain muted and we expect gradual improvement in domestic demand during the rest of the year on account of continued investments in infrastructure, healthy monsoons, favourable macros and festive demand. Commodities are likely to remain range bound.

PB Balaji, Group Chief Financial Officer, Tata Motors said:

“The first quarter has carried forward the momentum of last year with all businesses continuing to deliver on their distinctive strategies. We are confident of sustaining the performance in the coming quarters and delivering a strong year.”

| JAGUAR LAND ROVER (JLR) |

Highlights

- Q1 FY25Revenue at £7.3billion (+5.4% yoy), EBITDA 15.8%(-50 bps yoy), EBIT 8.9% (+30 bps yoy), PBT (bei) £693 million (+59% yoy).JLR’s highest Q1 revenue on record.

- Free cashflow for the quarter was £230 million.

- Net debt was at £1.0 billion, with gross debt of £4.8 billion.

- Total liquidity was £5.3 billion, including the £1.5 billion undrawn revolving credit facility maturing 1 April 2026.

Reimagine Transformation continues

Modern Luxury

- New RR Electric continues to generate strong global interest with c.41,000 sign ups to the waiting list.

- New Defender OCTA –the most powerful Defender ever made – initially revealed to a select group of prospective clients, at one of seven exclusive experiential events, prior to its public debut at Goodwood Festival of Speed, UK in July.

- Development of new Jaguar progressing well with camouflaged prototypes now in road testing.

Enterprise

- JLR increases investment from £15billion to £18billion over five years to support delivery of Reimagine

- JLR and Chery sign agreement for JLR to license the Freelander brand to CJLR joint venture for creation of portfolio of

electric vehicles in China, based on Chery’s EV architecture.

- JLR has trained 20,000 employees in electrification and digital skills to date; 95% of retail partner technicians now EV

trained in readiness for electric vehicle launches.

Sustainability

- Jaguar TCS Racing made history by becoming the Teams’ and Manufacturers’ World Champions of the 2024 ABB FIA Formula E World Championship, supporting EV technology and innovation for JLR.

- JLR is partnering with Pirelli to bring to market FSC‑certified natural rubber and rayon tyres, for use across JLR’s luxury vehicles at scale, debuting on the new Range Rover Electric

Financials

The positive momentum in JLR’s financial performance continued in Q1 FY25, driven by higher wholesale volumes, investment in demand generation and a favourable pricing environment. Revenue for Q1 FY25 was £7.3 billion, the best Q1 revenue on record, up 5% versus Q1 FY24. PBT (bei) in Q1 FY25 was £693 million, up from £435 million a year ago. EBIT margin was 8.9%, up 30 bps yoy. The higher profitability year-on-year reflects favourable volume, mix and material cost improvements, offset partially by increased marketing spend compared to a year ago.

Looking ahead

Looking ahead, we are likely to witness constrained production in Q2 and Q3 reflecting the annual summer plant shutdown and floods at a key aluminum supplier. As we work towards mitigation and recovery, we will hold our guidance on our key full year financial deliverables of >8.5% EBIT and achieving net cash.

Adrian Mardell,JLRChief Executive Officer, said:

“Thanks to the hard work and commitment of our people, JLR has delivered an outstanding set of results in the first quarter, with record revenues and an increase in year-on-year quarterly profits of nearly 60 per cent.We are making great progress delivering our Reimagine strategy. Our Jaguar TCS Racing Formula E Team, pioneers in electric technology innovation, are winners of this year’s ABB FIA Formula E Team and Manufacturer’s World Championships. We are bringing the lessons learned from this success on the racetrack to our luxury electric vehicles and later this year we will unveil our first next generation luxury electric vehicle, Range Rover Electric, which has more than 41,000 customers on its waiting list.”

| TATA COMMERCIAL VEHICLES(TATA CV) |

Highlights

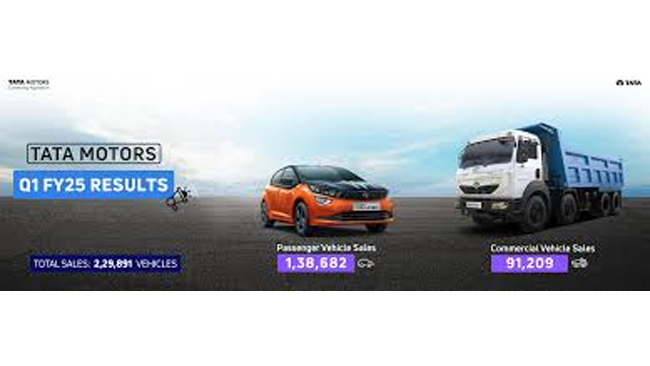

- Q1 FY25revenue at ₹17.8KCr, (+5.1%), EBITDA 11.6% (+220 bps), EBIT 8.9% (+240 bps), PBT (bei) ₹1.5K Cr.

- Q1 FY25 ROCE grows to 39.7% (36.5% in FY24).

- Q1 FY25CV segmentwholesales at 93.7K units (5.7% yoy). Domestic volumes grew 6.7% yoy whereas exports remained flattish.

- Domestic CV VAHAN market share at 39.0% in Q1 FY25.HGV+HMV 49.3%, MGV 39.2%, LGV 33.1%, Passenger 37.2%. Market share continues to strengthen in medium and heavies.

- Launched all new Tata Ace EV 1000, with higher payload capabilities and an extended range.

- Launched Fleet Verse, a digital marketplace across entire range of commercial vehicles.

Financials

During Q1 FY25 M&HCV segment led the growth.While HCV demand held up well, market sentiment remained positive in MCV segment with demand increasing in e-commerce, auto-aggregates and LPG segments. The volumes were up by 5.7% majorly driven by medium and heavy commercial vehicles. The revenues improved by 5.1% to ₹17.8K Cr. The business witnessed strong EBITDA and EBIT margins of 11.6% and 8.9%,respectively in Q1 FY25 lead by better realizations and cost savings and reported strong PBT(bei) of ₹1.5K Cr.

Looking ahead

The forecast of a healthy monsoon, expectations of policy continuity and continuing thrust on infra related developmental projects by the Government are expected to improve the demand for commercial vehicles. The demand in staff, intercity, and stage carriage segments should also remain healthy despite the seasonal dip often seen in school transportation in Q2 FY25. We will continue to drive our demand-pull strategy anddrive customer preferencethrough innovation, service quality and thematic brand activation.The business will continue to focus on strong EBITDA delivery, higher ROCE and unlocking value through downstream businesses.

Girish Wagh, Executive Director Tata Motors Ltd said:

“Q1FY25 registered a positive start for the Indian commercial vehicles sector. Tata Motors recorded commercial vehicles domestic sales of 87,615 units, ~7% higher than Q1FY24 sales. Overall positive market sentiment arising from increased economic activity, continuing infrastructure development, and growing demand of e-commerce, auto aggregates and LPG segments led to sales improving across most segments – HCV, MCV and CV Passenger. The business delivered strong EBITDA margins of 11.6% in Q1 FY25. Looking ahead, the widespread onset of monsoon, expectations of policy continuity in the forthcoming budget and thrust on infrastructure should be conducive towards improving overall demand for commercial vehicles. We will continue to drive our demand-pull strategy, step up customer engagement and improve competitiveness while closely tracking any emerging headwinds arising from interest rates, fuel prices and inflation.”

| TATA PASSENGER VEHICLES (TATA PV) |

Highlights

- Q1 FY25 revenue at ₹11.8KCr, (-7.7%), EBITDA 5.8% (+50 bps), EBIT 0.3% (-70bps), PBT (bei) ₹0.17K Cr.

- Q1 FY25PV wholesales at 138.8K units (-1.1% yoy).

- Q1FY25 EV volumesat 16.6K units (-13.9% yoy), due to sharp decline in fleet segment.

- EV penetration steady at 12%.CNG penetration increases from 16% in FY24 to to 22% in Q1 FY25.

- VAHAN registration market share held at 13.7% in Q1 FY25. EV marketshare at 67%.

- Tata Curvv, India’s first SUV Coupe unveiled, redefines mid SUV category.Set to be launched in August.

- Launched Altroz Racer – a sporty design combined with advanced tech.

- ev and Nexon.ev achieve 5 star Bharat-NCAP safety rating; Punch.ev records highest ever Bharat- NCAP score.

- Achieved a historic milestone with over 2 million SUVs on Indian roads.

Financials

PV business in Q1 FY25, after a boost in demand initially, saw a decline in retail (registrations) in the month of May and June, influenced by the general elections and heat waves across the country. Volumes stood at 138.8K units (-1.1% yoy) as we readjusted our wholesales in line with retails to keep channel inventory under control. Revenues stood at ₹11.8K Cr (- 7.7% yoy)on account of drop in volumes. Despite this, EBITDA margin improved50 bps yoy at 5.8%, on account ofmaterial cost reduction. EBIT margins declined by 70 bps yoy to 0.3% on account of adverse operating leverage,while PBT (bei) was at ₹173Cr.

Looking ahead

Although demand has remained less than anticipated, we expectit to pick-up during festive period.New product launches will augur well for the business.Our focus isto increase addressable market by introducing new nameplates, strengthen multi-powertrain strategy to leverage industry powertrain shifts and proactively grow the EV market in India while maintaining market leadership. We will work towards enhancing profitability through scale benefits, improving mix and optimization of cost & capex.

Shailesh Chandra, Managing Director TMPV and TPEM said:

“The Passenger Vehicle industry in Q1 FY25 witnessed retails (registrations) moderating, impacted by the general elections and intense heat waves across the country. Tata Motors sales of 138,682 cars and SUVs was slightly lower compared to Q1 FY24, as we proactively readjusted our wholesales in line with retails to keep channel inventory under control. Our multi-powertrain strategy and strong portfolio of SUVs led to steady sales. While the personal segment retails have grown for EVs, there was a sharp decline witnessed in the fleet segment. Going forward, we expect an improvement in overall sales on the back of the onset of the festive season and the launch of Curvv, India’s first SUV Coupe.”